by Rekha Balu, Aravind Boddupalli, Seema Agnani, ‘Alisi Tulua

The end of April marks the conclusion of National Fair Housing Month, in recognition of the passage of the Fair Housing Act in April 1968. But today, the legacy of housing policies and the ongoing work required to build and sustain prosperous, thriving communities remains. Most American families lack the resources to truly afford to live securely in their communities.

Recent findings from the Urban Institute and National CAPACD show this affordability crisis may be acute for some Asian American (AA) and Native Hawaiian and Pacific Islander (NHPI) families. This is especially true when it comes to housing costs. Our analysis finds that nationally, 33 percent of NHPI households and 29 percent of AA households are housing cost burdened (meaning they spend more than a third of their income on housing costs), compared with 22 percent for white households.

Affordability debates loom large in the US today, but they often lack the nuance needed to understand specific communities’ different experiences. With more disaggregated data and through partnerships with local community organizations, policymakers can implement better policy solutions to make housing more affordable for all AA and NHPI families.

Disaggregated data reveal stark gaps in housing cost burden

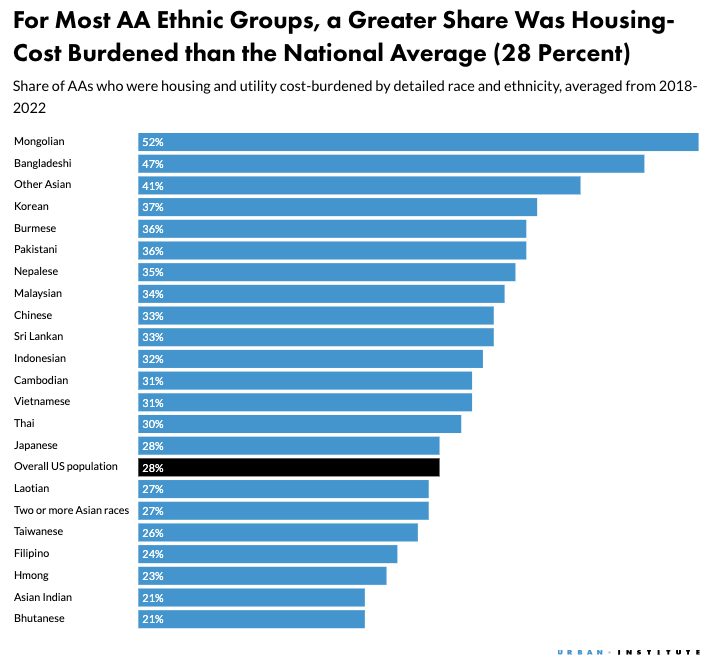

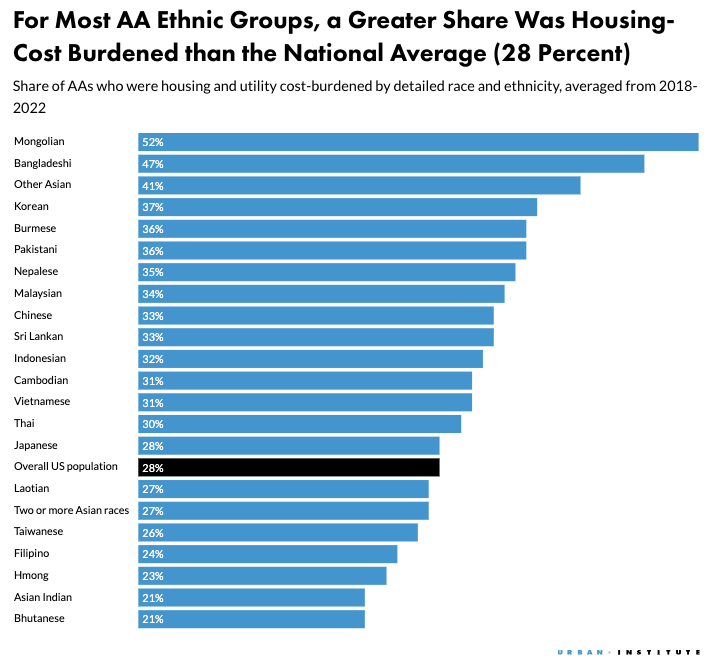

These economic challenges are more significant for some AA and NHPI racial and ethnic groups than others. More than a third each of Mongolian, Bangladeshi, and Korean people reported being housing and utility cost burdened in 2022.

Source: Urban Institute analysis of US Census Bureau 2018–22 American Community Survey public use microdata, downloaded from IPUMS USA.

Notes: These estimates include both homeowners and renters. For homeowners, housing costs include mortgage, property taxes, insurance, and utilities. For renters, costs include rent and utilities. Based on the federal guideline, households are housing cost burdened if they spend more than 30 percent of their incomes on these costs.

Higher housing cost burdens for AA and NHPI communities, overall, may reflect their concentration in high-cost metropolitan areas such as Los Angeles, New York City, and Seattle.

Source: Urban Institute analysis of US Census Bureau 2018–22 American Community Survey public use microdata, downloaded from IPUMS USA.

Notes: These estimates include both homeowners and renters. For homeowners, housing costs include mortgage, property taxes, insurance, and utilities. For renters, costs include rent and utilities. Based on the federal guideline, households are housing cost burdened if they spend more than 30 percent of their incomes on these costs.

Many fast-growing ethnic groups in the US, including Burmese, Nepali, Samoan, and Tongan communities, are concentrated in neighborhoods facing rapid rent increases, limited affordable housing preservation, and rising displacement pressures. When basic costs like rent require too much of a family’s income, it reduces their ability to save, invest, or build wealth. Urban Institute research shows that AA and NHPI communities have some of the widest within‑group wealth gaps of any major racial or ethnic group, underscoring how aggregated data can obscure major differences in access to opportunity.

How state and local housing programs can support AA and NHPI communities

Most city and state housing programs do not routinely collect outcome data disaggregated by race and ethnicity, making it difficult to evaluate whether specific programs are benefiting AA and NHPI communities.

Our evidence provides some initial guidance for improving stability:

- disaggregating data and findings, both by racial or ethnic group and metropolitan area or neighborhood to identify who is experiencing worse or better outcomes

- identifying opportunities for preservation and development of affordable housing, especially in high-cost metropolitan areas

- engaging culturally rooted housing organizations and community-based developers to identify solutions targeted to their communities, though changemakers may need to be cognizant of the evolving legal jurisprudence and political landscape.

Luckily, some promising interventions are on the way. Mayor Karen Bass recently announced a $1 million grant through the Los Angeles County Affordable Housing Solutions Agency’s Renter Protection and Homelessness Prevention Program to a collaborative of 11 community-based organizations to support housing stability for vulnerable AA and NHPI households, part of a comprehensive plan to protect renters and prevent homelessness.

With so many different AA and NHPI communities in Los Angeles, the city could consider a collaborative approach that includes community-based organizations that serve as trusted messengers, have linguistic and cultural competency, and are able to offer a variety of rental assistance, legal support, and stabilization services. This approach can be especially effective in helping families stay housed and preventing homelessness.

For example, the Southern California Pacific Islander Community Response Team, 1 of the 11 organizations in the collaborative, provides resource navigation services and coordinates a group of 17 regional NHPI-serving organizations to effectively reach the diverse NHPI community in Los Angeles, as well as other communities with the highest housing cost burdens.

Without disaggregated data to inform needs, government funds may have gone to one organization, serving only a small part of Los Angeles’s diverse communities. However, with the insights and understanding of the community at the city and neighborhood levels, the breadth of the Los Angeles residents may now be better served to prevent homelessness.

A path forward

Our research points to the importance of leveraging insights from disaggregated data to inform policies that improve affordability.

Policymakers at the national, state, regional, and even citywide levels can lean on the data and partner with the local organizations most likely to have the knowledge and cultural competency to design and implement effective solutions for all families.